Predicting the future for Metal Injection Moulding

In a Special Interest Seminar titled ‘The Future of MIM’, at the Euro PM2019 Congress, organised by the European Powder Metallurgy Association (EPMA) and held in Maastricht, the Netherlands, October 13-16, 2019, an analysis of the current status of Metal Injection Moulding (MIM) technology and predictions for its future development were provided in a presentation from Benedikt Blitz, Managing Director, SMR Premium GmbH, Germany.

SMR Premium is a member company of the SMR Group and specialises in the provision of market intelligence for High Value Materials. Powder Metallurgy production is one focus of the company’s materials portfolio. This report focuses on Blitz’s assessment of MIM, in keeping with the presentation’s title, although other powder-based processes, such as HIP and Additive Manufacturing, were also considered during the presentation.

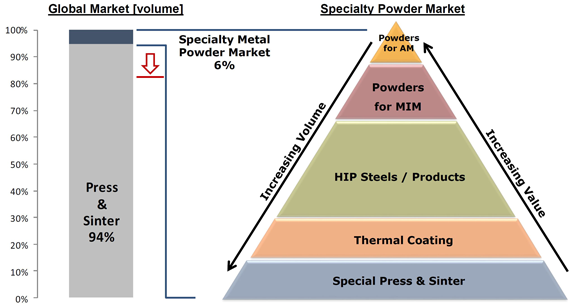

Blitz began with a short overview of the global steel industry, which identified that the total annual tonnage of all PM processes (~1.3 million tonnes) equates to less than 0.1% of total steel product tonnage (~1,800 million tonnes). The presentation emphasised that 94% by volume of metal powders is consumed by conventional ‘press & sinter’ Powder Metallurgy, but, for the remaining 6% (including MIM powders), the tenet is to concentrate on value rather than volume and target the high end of the market (Fig. 1).

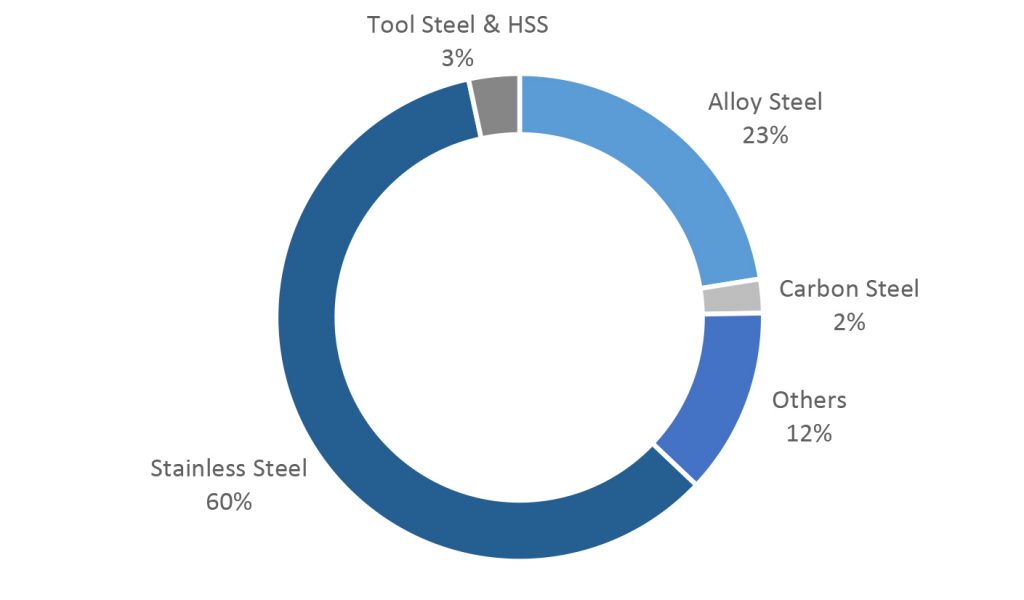

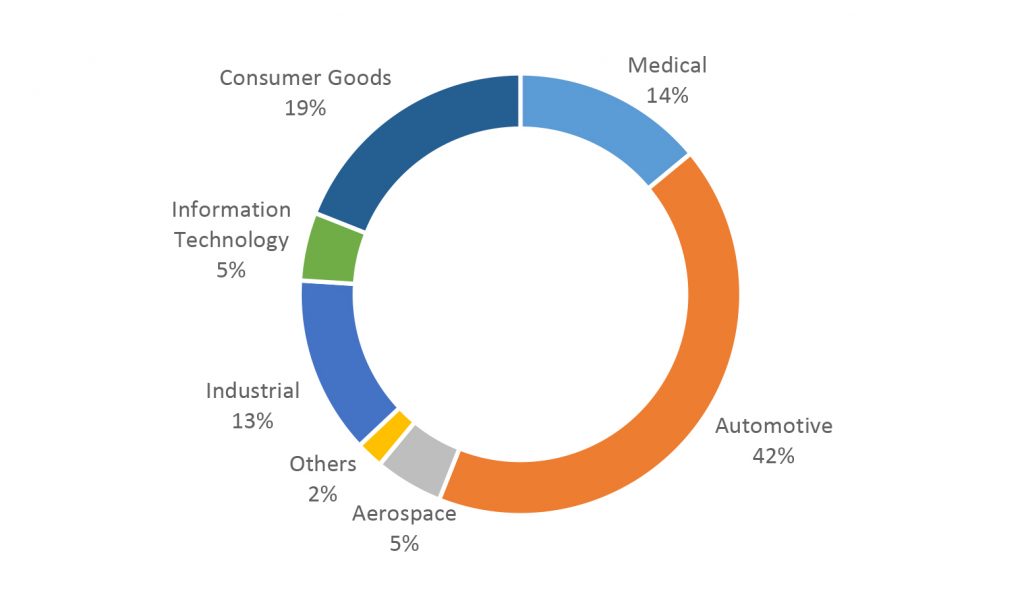

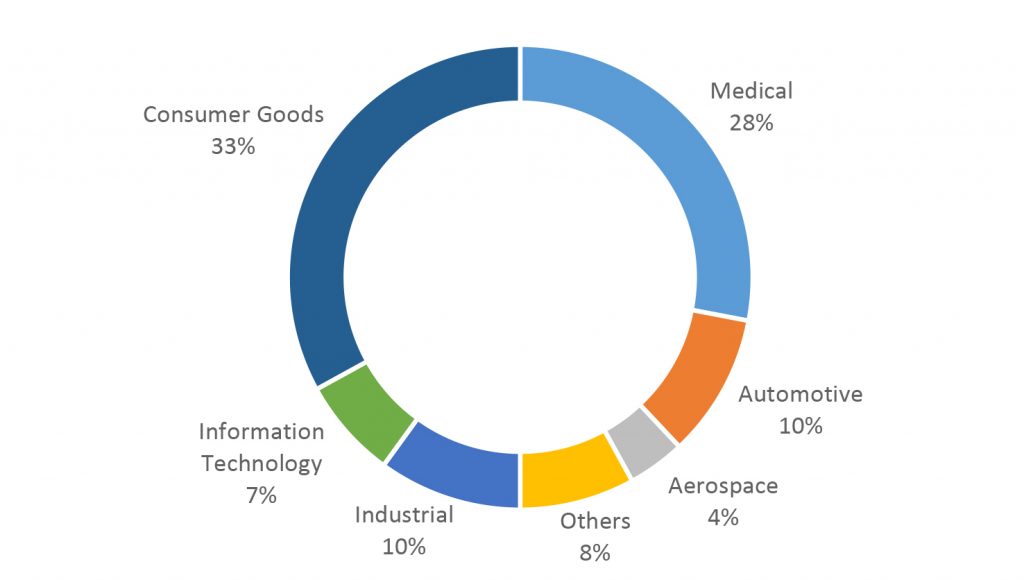

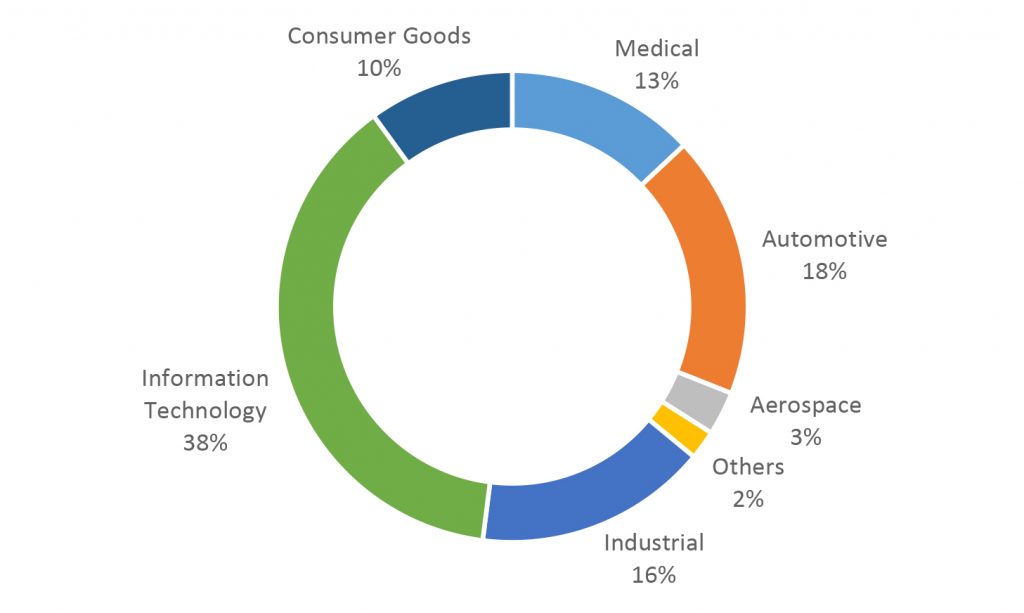

In describing the current status of MIM, data were provided (Fig. 2) on the breakdown of products by material type and customer sector. In relation to powder type, stainless steels account for 53% by volume, other steel types 25%, superalloys 11% and a variety of other metals 11%.

Fig. 2 Current global MIM applications by material type and end-use sector (Courtesy Benedikt Blitz / As presented at Euro PM2019)

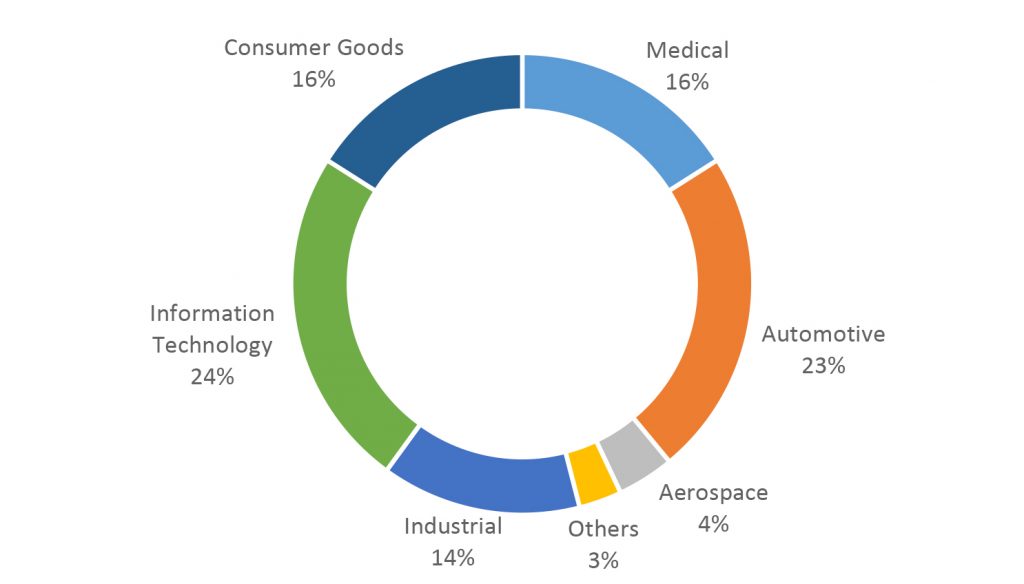

The global breakdown by industry sector revealed a broad range of applications. The application breakdown by geographical region shows significant differences; in Europe, automotive applications are relatively dominant; in North America, medical and consumer goods; and, in Asia, information technology (Fig. 3).

An analysis of MIM products by weight and size emphasised that they are currently predominantly small parts. Data were also provided to divide the global totals for sales turnover (~€2,300 million) and active parts producers (630) by geographical region, emphasising the significant role of China.

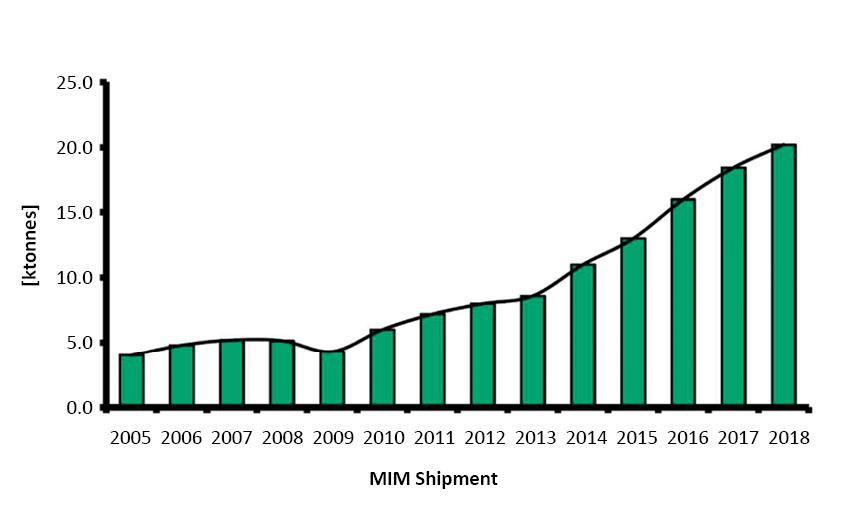

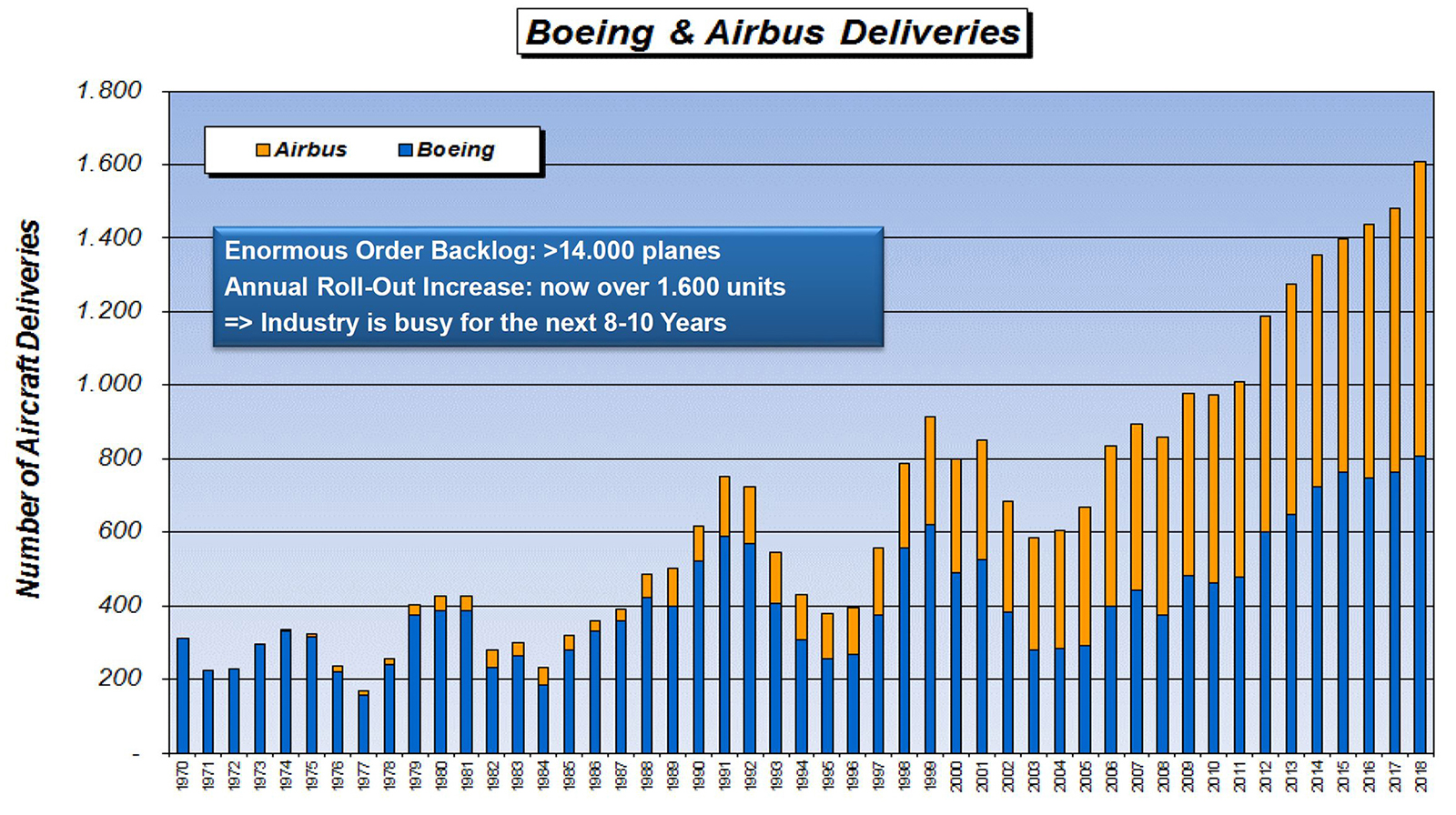

It was then emphasised that the widespread markets for MIM products mean that these applications are encountered in every aspect of daily life, particularly in transportation, aerospace, the 3C industry and a broad range of consumer products. In relation to the future market developments, it was predicted that the significant rise already observed in production levels for Boeing and Airbus will continue more strongly over the next eight-to-ten years (Fig. 4).

Fig. 4 Predicted growth in aerospace demand (Courtesy Benedikt Blitz / As presented at Euro PM2019)

Finally, an overall summary of SMR’s predictions for PM global market evolution by manufacturing technology type up to 2025 was shown. MIM is predicted to show a compounded annual growth rate (CAGR) of around 11% over the period. This was second only to the predicted growth rate for AM (25%), although, of course, AM is starting from a much lower base level. These figures can be compared with the predicted CAGR for Press & Sinter PM, the traditional bedrock of the PM sector, of only around 3%.

In terms of MIM market development by end-use sector and geographical region, the predicted growing significance of automotive applications and demand in China was also emphasised.