WorldPM2026: MPIF president sees PM industry entering transformative period

The annual ‘State of the PM Industry in North America’ address was presented by the Metal Powder Industries Federation’s (MPIF) President, Christopher Adam, at the 2026 Powder Metallurgy World Congress (WorldPM2026), held in Montreal, Canada, June 26-29. During his overview of the wider industry, Adam reviewed developments in Press and Sinter PM, Metal Injection Molding, metal Additive Manufacturing, and Hot/Cold Isostatic Pressing.

“The global Powder Metallurgy (PM) industry is navigating what can best be described as a period of ‘glorious uncertainty,’ driven by political upheaval, trade disruptions, technological shifts, sustainability challenges, and geopolitical conflict,” stated Adam. “These forces are reshaping metal powder technologies, including conventional press-and-sinter PM, Metal Injection Molding, and metal Additive Manufacturing.”

“A major disruptor has been tariff volatility. The imposition, invalidation, and restructuring of US global tariffs, along with sector-specific steel and aluminium duties, have created significant uncertainty in pricing, contracts, and supply chains. Companies are being forced to renegotiate supplier and customer agreements while reassessing sourcing strategies. For conventional press-and-sinter PM, which depends heavily on global powder flows, tariff shocks and legal reversals have made long-term planning difficult. At the same time, reshoring efforts, particularly in rare earths and magnet production, are opening domestic growth opportunities,” continued Adam.

China’s recent export controls on rare-earth materials, coupled with US restrictions on Chinese-origin rare-earth magnets beginning January 2027, are accelerating investment in domestic mining, alloying, and magnet manufacturing.

“The US capacity could reach 30,000 tons annually by 2030, but faces higher costs, demand uncertainty, and heavy rare-earth processing chokepoints,” added Adam. “As the projected capacity benefits PM producers of magnetic materials, tungsten, and refractory metals, a critical shortage of skilled labor and environmental concerns in mining, chemical processing, and magnet manufacturing threaten to slow expansion.”

Press & Sinter Powder Metallurgy

The automotive industry is the largest consumer of iron powder, but market dynamics are shifting, stated Adam. “While earlier forecasts anticipated rapid electrification, EV momentum has cooled amid government policy reversals and weaker-than-expected demand. Numerous EV programs have been cancelled or delayed. Ford discontinued the F-150 Lightning pickup, Ram cancelled the electric 1500 truck, Tesla is about to discontinue the Model S and Model X, and the Chevrolet BrightDrop van has been retired. The list of paused, cancelled or delayed EVs keeps growing, and General Motors has paused its battery production for facility upgrades.”

Adam highlighted that the rising passenger vehicle prices, elevated interest rates, and increasing insurance and repair costs are making new vehicles less attainable for lower-income households. Many price-sensitive consumers are being pushed out of the new-car market altogether, he said. In contrast, higher-income buyers continue to drive sales, particularly in hybrid vehicles and higher-margin models, helping to sustain overall market demand despite broader economic pressures.

“This shift in purchasing dynamics carries important implications for the PM industry, which remains closely tied to automotive production volumes and vehicle mix. A market increasingly weighted toward premium and hybrid models may influence both material demand and component requirements.”

However, there are encouraging signs for improved affordability, Adam was keen to point out. Several automakers have announced plans to expand their lineup of lower-cost vehicles in the coming years, and Stellantis, for example, has indicated it intends to introduce nine North American models priced under $40,000 by 2030, he said. Such initiatives could help broaden consumer access to new vehicles and provide renewed momentum for automotive-related manufacturing sectors, including PM.

“More than 70% of North American iron powder shipments go to passenger vehicles, underscoring the sector’s reliance on automotive demand,” Adam stated. “Improving fuel efficiency – through enhanced engine performance, lightweighting, and alternative power systems – will remain a priority for both internal combustion and hybrid vehicles. Although lightweight materials such as aluminium and titanium are gaining traction, ferrous alloys are expected to retain dominance due to their strength and cost advantages.”

It was shown that in 2025, the average North American passenger vehicle is estimated to contain about 14.3 kg (31.5 lb) of PM components, a slight decline from prior years. It is hoped that as market conditions shift and automotive design and manufacturing evolves, this will create new opportunities for the PM sector. “However, PM should continue strong R&D activities to look for new and emerging markets. Production of new battery materials and energy storage devices is expected to grow for both EVs and stationary electric storage facilities. This can be a new high volume growth area for PM,” added Adam.

Metal Injection Molding

“Metal Injection Molding continues to demonstrate resilience,” Adam was keen to highlight. “Industry surveys show cautious optimism, with growth concentrated in medical and stainless steel applications, even as firearms demand softens. MIM’s core strength, high-volume production of complex geometries, remains intact.”

However, it faces challenges from tariffs, labor shortages, inflationary pressures, and overseas competition, added Adam. Updated MPIF material standards and engineering data are helping strengthen design confidence and quality compliance, and many believe the MIM industry is about to begin its recovery.

Metal AM

“Metal AM remains promising but turbulent. After years of heavy investment and hype, the sector has faced consolidation and high-profile bankruptcies. Most of the metal AM success has been led by powder-bed-fusion (PBF) and directed-energy deposition (DED) processes, where the industry has shifted from prototyping to production, qualification, and implementation.”

However, high capital costs, raw material prices, and technical hurdles have slowed adoption.

“Nevertheless, innovation continues in binder development, hybrid additive-subtractive systems, cold spray-based processes, and AI-assisted process optimisation,” stated Adam. “AM currently complements MIM in prototyping and low-volume production but will become more competitive if productivity and reliability improve.

Global impacts

Geopolitical conflicts, including the war in the Middle East and ongoing Russia-Ukraine conflict, are increasing defence demand for refractory and hard materials while driving energy price volatility. Oil, gas, mining, and strategic materials exploration are expanding, creating new opportunities for PM in wear parts, tungsten carbide, and energy infrastructure.

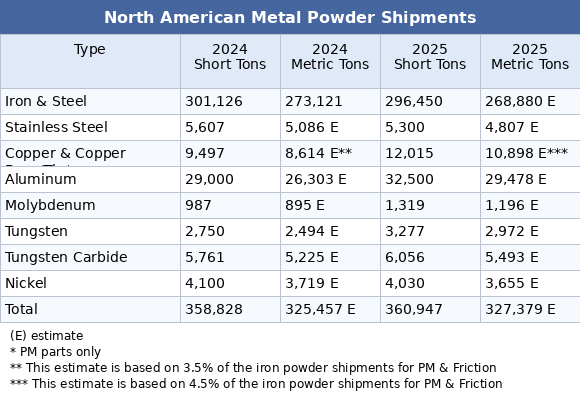

It was stated that the total estimated 2025 North American metal powder shipments was very similar to the previous year, with a slight increase of 0.6% to 327,379 mt (360,947 st).

“North American iron powder shipments have traditionally served as the most reliable indicator of the PM industry’s overall health,” Adam added. “However, moving forward, reported shipment data will be based on estimates, as only two major iron powder suppliers remain in North America. Total iron & steel powder shipments decreased 1.6% to 268,880 mt (296,450 st).

Estimated aluminium powder shipments for 2025 rose 12.1% to 29,478 metric tons (32,500 short tons). However, it was pointed out that this increase largely reflected a correction of previously understated shipment figures, rather than true market growth.

Copper and copper-base powder shipments increased by 26.5% to 10,898 metric tons (12,015 short tons). The rise was primarily attributed to inventory stabilisation following the consolidation of two separate facilities into a single operation, rather than a significant increase in underlying demand.

Estimates for nickel shipments decreased 1.7% to 3,655 mt (4,030 st); stainless steel powders, decreased 5.5% to 4,807 mt (5,300 st).

Estimates for molybdenum increased 33.6% to 1,196 mt (1,319 st); tungsten increased 19.2% to 2,972 mt (3,277 st); and tungsten carbide powder increased by 5.1% to 5,493 mt (6,056 st).

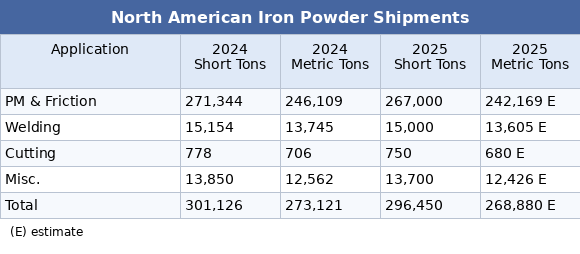

PM and friction-grade iron powder shipments declined 6.5% to 246,109 mt (271,344 st). Welding applications decreased by 1.8% to 13,745 mt (15,154 st). Cutting, scarfing, and lancing applications decreased by 13.9% to 706 mt (778 st). Miscellaneous uses were flat.

MIM and metal AM powders

“The MIM and metal AM spherical powder producers experienced continued shipment declines in early 2025, extending a downturn that began in 2023,” claimed Adam. “The slowdown was largely attributed to excess inventories accumulated during prior years when purchases outpaced consumption. In addition, the increased reuse of print and build-bed powders in AM processes reduced the need for new powder purchases, further dampening demand. Feedstock producers, among the largest consumers of spherical metal powders, also contributed to market instability by maintaining substantial raw powder inventories to safeguard supply continuity for their customers. While this strategy ensured production reliability, it suppressed new powder orders and prolonged the correction cycle across the supply chain.”

Despite the challenging start to the year, it was stated that many industry experts reported that market conditions began to improve in the second half of 2025. Inventory levels gradually normalised, and order activity strengthened. “Powder producers are increasingly optimistic that the recovery will continue through 2026 and beyond, with some anticipating sustained double-digit growth if demand trends hold.”

Stainless steels, low-alloy steels, and titanium remain the core materials used in MIM applications. However, Additive Manufacturing has significantly broadened the material landscape, stated Adam. “AM technologies enable greater use of aluminium, copper, titanium, tungsten, and a growing range of specialised alloys, expanding opportunities across multiple industries,” he said.

“Demand growth is particularly strong in aerospace, defence, and medical sectors, where performance requirements and design complexity favour powder-based manufacturing technologies,” Adam said.

“Combined North American metal powder shipments for MIM and AM are estimated to have increased by approximately 5% in 2025, signaling early recovery,” continued Adam. “While some industry insiders described 2025 shipment levels as comparable to the prior year, there is broad consensus that 2026 will deliver more meaningful growth as inventory corrections subside and end-market demand strengthens. With improving conditions and expanding application opportunities, the MIM and AM metal powder sector appears positioned for a more robust growth phase in the years ahead.”

Tungsten & molybdenum

It was highlighted that in February 2025, China imposed export restrictions on dual-use tungsten materials, authorising only fifteen domestic companies to export these products. At the same time, China sharply increased its global purchases of ore concentrates, raw materials, and scrap, intensifying supply pressures. Within months, the global market experienced a severe shortage of tungsten raw materials, reported Adam. The ammonium paratungstate (APT) price index surged from approximately $325 per metric ton unit (MTU) to nearly $3,100 per MTU. As a result, tungsten and tungsten carbide (WC) powder prices rose by roughly eight to ten times their previous levels.

“US tungsten refiners responded by increasing chemical production to full or near-full capacity,” he added. “However, this expansion proved insufficient to meet domestic demand for tungsten and WC powders. Downstream producers of sintered components struggled to secure adequate supply, and many US companies that had previously relied on Chinese sources remained cut off. Elevated prices further constrained the market, leaving some part manufacturers unable to afford essential raw materials.

Meanwhile, accelerating global growth in artificial intelligence and data centers boosted semiconductor production, increasing demand for high-purity tungsten powder. Rising electricity consumption also spurred construction of multiple prototype fusion reactors, each requiring substantial tungsten volumes, added Adam. US defence demand rose sharply in 2025 and continued into 2026 amid global conflicts. Molybdenum demand similarly increased, driven by military, aerospace, and space applications, while traditional industrial uses remained steady with modest growth.

The outlook

“In many ways, the PM industry is being tested and defined, at this moment,” continued Adam. “Conventional press-and-sinter continues to benefit from hybrid vehicle demand and defense growth, even as supply-chain uncertainty tempers optimism. MIM remains steady but measured, balancing opportunity with caution. Metal AM offers unbridled potential but must still clear financial and technical hurdles before it can be fully scaled. Across every platform, the fundamentals remain the same: strong workforce development, resilient supply networks, and sustained investment in R&D will determine who leads in this volatile era.”

“But challenges and opportunities often arrive together. The PM industry stands at the threshold of meaningful transformation, with the tools, expertise, and ingenuity to chart new pathways for growth. By embracing sustainability, accelerating technological advancement, and deepening collaboration across sectors, we can turn uncertainty into momentum. Advancing metal powder technologies will not only unlock new applications, but it will also strengthen our collective position in a rapidly evolving manufacturing landscape.”

“The sky is the limit! Rare-earth sintered magnets; drones; humanoid robots; energy storage; thermal management; soft-magnetic-composites (SMC) for electric motors; surgical instruments; wearable devices; turbocharger components; small complex aerospace components; fuel nozzles; nuclear components; and manufacturing tools are all opportunities for metal powder technologies.”

“The PM industry needs to seize opportunities when they arise and be bold enough to create them when they don’t. I am confident that our industry is well positioned to meet the evolving needs of our customers and to rise to the challenges ahead with resilience and innovation,” concluded Adam.