Strong year recorded for China’s MIM industry in 2019, with smartphone production continuing to drive growth

A survey conducted by the Metal Injection Moulding Committee of the China Powder Metallurgy Alliance (CPMA) has revealed that the MIM industry in China continued on a rapid growth track in 2019. The total sales volume of MIM parts in China (excluding Taiwan), was estimated to be RMB 6.7 billion, up by 17.5% on 2018. These sales were primarily driven by the 3C sector. In addition, smart wearable devices, micro-gearboxes, hardware and automotive parts contributed to growth.

There are currently over two hundred MIM firms operating in China, among which two companies report sales above RMB 1 billion. Ten companies are reported to have achieved sales of more than RMB 100 million.

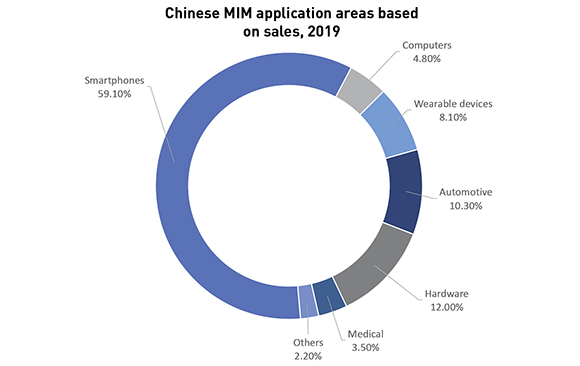

Components for smartphone applications continued to dominate the market, with modest growth reported, whilst the demand for components for smart wearable devices continued to grow. There was, however, a drop in the market share for parts for computers and medical devices. Application areas, by sales value, are shown in Fig. 1.

In 2019, the total volume of MIM powder sales recorded was approximately 10,000 tons, 15–20% higher than that reported in 2018. There is recognition, however, that MIM grade powders are now also being sold to the growing Additive Manufacturing industry, potentially affecting these figures. With regards to MIM feedstock production, the survey found that the market share of domestic Chinese feedstock brands has risen to around 65% of the entire market. Of the international producers, BASF SE’s Catamold catalytic debinding feedstock continues to dominate.

Stainless steels continue to dominate production, accounting for 70% of the market by weight. Low-alloy steels account for 21%; cobalt-based alloys 6%, and tungsten-based alloys 2%. The balance includes titanium, copper and cemented carbides, to name a few.

Outlook

The CPMA states that, driven by the efforts and technological progress of China’s MIM industry, the overall awareness of MIM in China is steadily improving.

In terms of material performance, dimensional tolerances, production efficiency and manufacturing costs, as well as labour protection and environmental impact, MIM is achieving a comprehensive competitive advantage over the investment casting and CNC machining industries. As a result, MIM is expected to be used for new applications in the automotive sector, for both conventional and electrified vehicles.

In the 3C sector, new folding screen devices, including both smartphones and tablets, will appear in the market during 2020 and the industry estimates that folding screen penetration will reach 5% of the market. More broadly, smartphone manufacturers will increase their use of MIM products, bringing new growth opportunities.

The survey’s authors concluded that, propelled by 5G technology and the progress of IoT (the Internet of Things), MIM products will continue to embrace a wide range of new opportunities. Moreover, it was stated that the introduction of metal Additive Manufacturing is likely to give a further boost to the industry.